The 4 horsemen of Government debt have come knocking

And the last 40 years of investing is dead?

Good Morning Decentralized Way subscribers! And my apologies for the delay between articles… I promise this one is worth the wait.

As I’m sure you’re sick of hearing, we live in ‘unprecedented’ times. Or so they say. But it’s really not true, at least not from a monetary standpoint. We’ll unpack this further in a later article to keep this one short (ish).

However, if you’re under the age of ~81 or so (and really more like 95+ since it’s unlikely you started paying attention to monetary policy straight out of the womb), these are unprecedented times to you. And me.

But history truly does rhyme because humans react in similar ways time and time again. So a trip back in time is required to understand what is happening today.

So with that, let’s hop right in.

The mantras and principles of the last ~40 years of investing are dead

Whoa. Bold claim, I know. But here’s why.

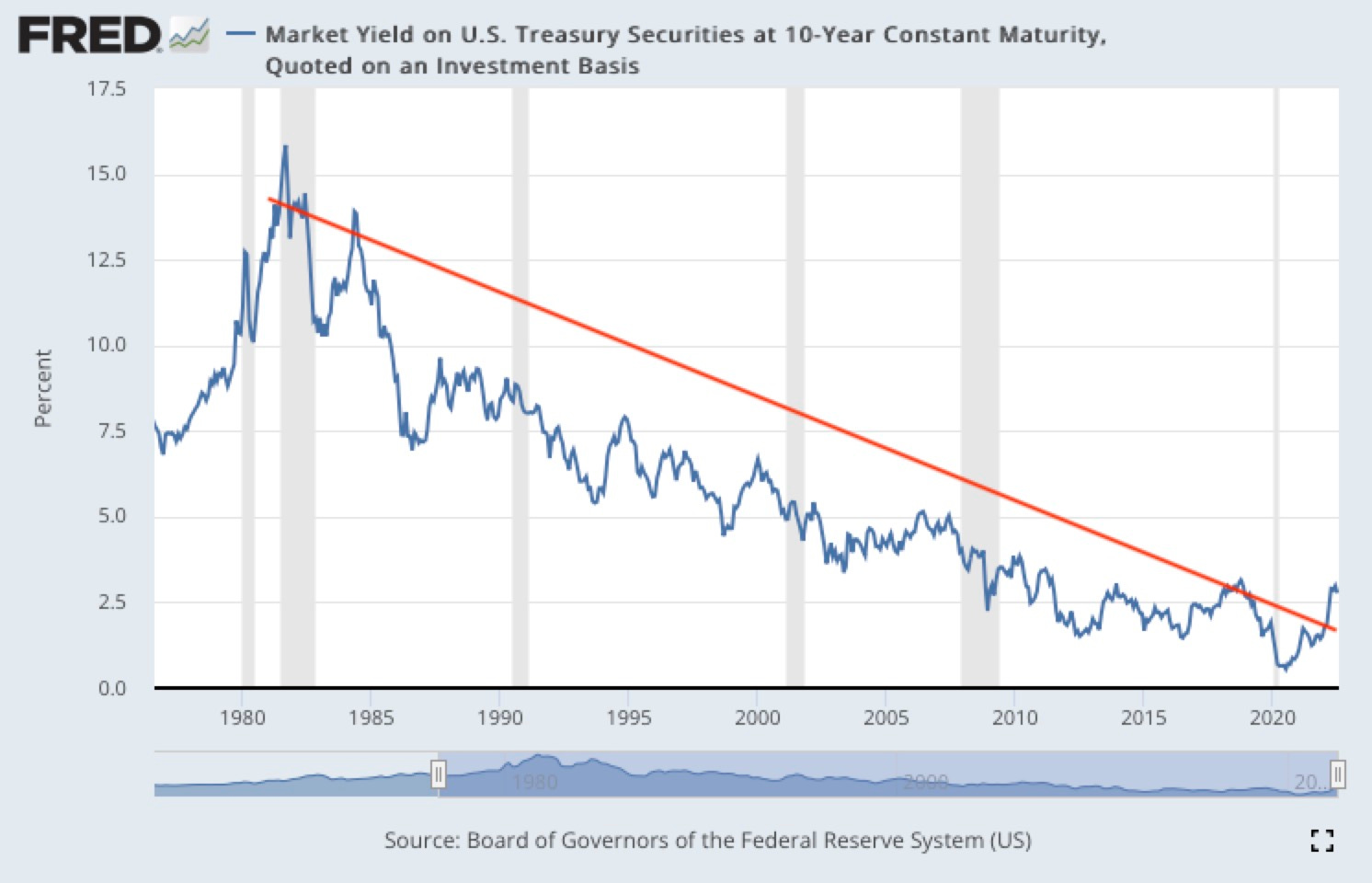

In simple terms, the chart below shows the interest rate on US Treasuries. Source. I’ve taken the liberty of drawing a not-so-precise trend line on there for you.

But why does this matter? It shows that since the early 1980’s, interest rates have been declining. In broad terms, it means that since the early 1980’s, it has gotten cheaper and cheaper to borrow money.

You’ll notice that trend line has now been broken. When rates fall consistently, investors get comfortable with the status quo. Businesses take on more debt, grow faster, profits rise, and everyone wins. Falling rates create bull markets, otherwise known as conditions where pretty much every asset rises in price. If you closed your eyes and threw a dart at the board, you probably made money.

Everyone is a genius in a bull market.

But this can’t continue forever. And when this trend changes, so does everything you thought you knew about investing over the last 40 years.

No longer are growth stocks able to take on dirt cheap VC money to fuel them. No longer can unstable businesses pull a Theranos and not have investors truly dive into their balance sheets or products.

No longer can assets meteorically rise in price for 40 straight years because an increase in rates destroys demand. This applies to equities, real estate, and every other category you can think of. We’ll touch on what the Fed and rates are doing towards the end of this article.

Once rates reach ~0%, there’s really no more room to go down (unless you’re the European Central Bank and you go negative and pay people to borrow). They must either stabilize or rise - both of which break the trend line.

Ok so it’s gotten cheaper to borrow money and that looks like it’s changing, but why does that matter?

Cheap money = loading up on debt

If you walk into your local grocery store and find that your favorite brand of tortilla chips are on sale, what do you do?

Well you load up of course! The more the merrier!

And if you walk in the next week and they’re even cheaper, what do you do?

Well you get more! You’ll eat them eventually, right?

And debtors do the same. Namely the biggest debtor of all, the US Government.

Here’s a chart of the total public debt, approved and spent by your friends in Washington. Source.

Do you notice anything funny?

Namely that it rises exponentially, starting in the early 1980’s or so?

And if you scroll up to our first chart, you’ll see that interest rates started falling in the early 1980’s… Curious isn’t it?

Wondering how are these things are connected?

More debt + falling rates = no problem!

During the past four decades, the increase in debt over time was always offset by reductions in interest rates, so that the cost of servicing that debt never really went up.

Go read that sentence again and then we’ll unpack it.

Now breaking this down in simple terms. Servicing debt is a fancy term for making interest payments on the money you owe - think car payment, mortgage, etc. If you fail to service your debt aka make your interest payments, you default. No bueno.

Let’s use a mortgage as an example with simple numbers. Imagine if you owed $50,000 dollars in total and you’re paying $100/month to service your debt on your home. To kind of mimic the ways government debt is financed, let’s say you have a variable interest rate.

Now imagine that you found out you could buy another home for $50,000 and your payment would stay the same. Sounds crazy right?

Hint: it is.

But that’s exactly what our policymakers have done over the last 40 years of falling interest rates. To use our example, they’ve taken on more and more houses (debt) and modified the interest rates so that they don’t have to pay any more money per month.

Please keep in mind - This is overly simplified of course - but the principles remain the same.

So now you’ve done this process over and over and you ‘own’ 5 houses and you’re still just paying $100/month! Life is great, right?

Well as my dad would say, there’s no such thing as a free lunch.

Note my use of ‘own’ above. You don’t really own those homes. The bank does. And when interest rates rise, your payment now becomes $500/month! You can’t afford that and you go bust. You default on your obligations because you can no longer service your debt.

The bank takes the loss and if it’s anything like 2008, the government bails them out, creating more public debt in the process.

But what happens when it’s not your debt - it’s the government itself?

Well, going broke isn’t an option for those in power. So what is?

The 4 horsemen of Government debt. You must choose at least one. What will it be?

Austerity. Otherwise known as spending less. A reasonable solution you’d think? But not for central bankers and politicians because it’s too painful. Spending less means people’s lives get worse, which breeds instability, which leads to unrest. Not an acceptable outcome for the powers that be since that would risk their power itself. Can’t have a French Revolution.

Debt defaults & restructuring. You thought spending less was painful? Ha! This is that pain on steroids! Understand this - debts are someones assets. Meaning if I loan you $10, you owe me that $10 back (plus some interest of course). I can count that $10 loan as an asset on my balance sheet. Defaulting means that you don’t have to pay… But it also means that I don’t get paid. Moral of the story, someone has to eat the loss. Not fun for anyone and not an option for the powers that be.

Transfers from ‘haves’ to ‘have nots’. If you read the news, even occasionally, you’ve seen movements to ‘tax the rich’ and corporations and such. Regardless of political affiliation, this is typically part of the ‘solution’. But it never generates enough money so…

Printing & devaluing money! Ah we’ve finally arrived, but you knew we were headed here all along. Printing and devaluing is the fastest and least understood method because it’s hidden behind terms like quantitative easing. Everyone sees asset prices rising and thinks this must be a good thing! But more importantly, it’s very difficult to identify the ‘harmed’ parties until it’s much too late. History shows that this is the path always taken by indebted governments.

To summarize the 4 horsemen…

Cutting government spending (likely on social programs first before politicians salaries, of course) hurts the poorest people directly.

Raising taxes on the rich and corporations is met with resistance because it’s perceived as taking money out of their pockets. Those same individuals also lobby congress to not take this course of action, and data shows they’re very successful at doing so.

Debt defaults harm everyone because it destroys confidence and willingness to spend and loan money. The whole system as you know it comes crumbling down if this happens.

But quantitative easing? Yeah sure! Nobody really knows what that means anyway! And a look through the history books shows that this is the option chosen time and time again by rulers in financial trouble.

And it takes money directly out of your pocket

In other words, debt monetization. Big words with equally big implications.

If the government can’t afford to pay back the debt, they’ll simply just print money to make it happen.

For this, understand the difference between number of dollars and purchasing power. Number of dollars is self explanatory, but purchasing power is what you can buy with those dollars. If $10 only buys me 1 gallon of gas, then $10 ain’t worth much. But if $10 buys me a full tank, then I’m feeling pretty good about that $10.

The key here is that it’s still the same $10 numbers wise. So let’s apply this to government debt.

Current public debt is at ~$30 trillion dollars. That’s $30,000,000,000,000. An absolutely unfathomable number.

The powers that be have no choice. They’ll simply print however much they need on a given day to service the debt and keep the charade going. They’ll literally add zeroes to an Excel spreadsheet.

They’ll ‘pay it back’ by printing. So the creditors get their $30,000,000,000 in terms of numbers on a screen… But it isn’t really worth anywhere near that much in terms of how we think about purchasing power today.

But what does this mean for you?

It means that inflation will be a mainstay throughout your lifetime. It’s not going anywhere even if it subsides from current levels because the numbers simply don’t allow it. And that means your money is worth less and less. There’s two solutions. One, travel back in time to pre 1971. Or buy Bitcoin. The only form of money ever invented that cannot be manipulated by human greed and short sighted decision making.

But what if the Fed sticks to QT?

You may have seen some news about the Fed reversing course to quantitative tightening, aka reducing the money supply.

Well, if the Fed stays the course, we’ll have extended periods like the red zones below. Those are even more painful than the inflationary periods, but they’re unfortunately necessary due to how our system of expansionary credit works. More on this another time.

But as we discussed above, the powers that be have no choice but to print money to keep the charade going. So even if the Fed sticks to QT and reducing the money supply for a short period, they’ll inevitably have to reverse course back to QE and printing money, otherwise they risk default.

Meaning asset prices will once again rise… Once the Fed gives them permission.

The takeaway? Don’t fight the Fed. If they say QT and raise rates, buckle up. If they say QE and cut rates, toss a dart at the board.

Where do we go from here?

History shows us that there are stages to short term and long term debt cycles and we’re nearing the end of a long term debt cycle that will likely be painful. It’s only by printing money that the powers that be kick the can down the road. And kick it they are.

Stay tuned to your inbox as next up we’ll be unpacking short term and long term debt cycles as well as discussing what happens when dollar strength rises.

And as always, we’ll dive into how these macro movements affect you.

And with that, go get yourself some Bitcoin and I’ll see you in the next edition of the Decentralized Way.

Very informative, as always 🤝

really creative of you to use the horsemen framework! great piece.