The US dollar is actually gaining strength?

How the Japanese bond market helps us understand US dollar movement

Good afternoon Decentralized Way subscribers!

I’ve seen a lot of chatter about the US dollar and it’s strength in the past couple days, and it’s true! The US dollar hit its highest level in 6 years last week.

While that may be the headline you see, you know by now that it doesn’t tell the full story.

Maybe you’re wondering if this means inflation isn’t actually 8%+ (officially) or 15%+ (unofficially)?

This article will take us from the Fed, to South America, over to Europe, stopping in Japan, through some bond markets, and back to the Fed again. All in just a few minutes.

And with that, away we go.

Note - To prevent putting source tags next to every currency statistic, all currency information and statistics come from this source.

What is DXY?

DXY is the US dollar index, created in 1973 by the Fed (yes, them again) to provide a measure of the US dollar versus other foreign currencies.

When you hear newscasters say that the dollar hit an all time high, they’re talking about DXY, meaning that the dollar is at an all time high compared to other currencies.

But this doesn’t necessarily mean that the dollar is truly gaining strength. Maybe it’s just the best of the worst? Let’s find out.

The sharpest crayon in the box (kind of)

Read these next two lines carefully.

If DXY rises, it doesn’t necessarily mean that money is flowing directly into the dollar. It could also mean that demand for other fiat currencies is falling against the US dollar.

That’s the case here, mostly. (Adding the ‘mostly’ because as with anything in macroeconomics, there is never simply one factor at play).

Understand that there is no ‘absolute’ benchmark. When comparing currencies, the only thing you can compare them to is themselves. In this case, the dollar is perhaps just the sharpest crayon in the box. Still a crayon though.

With that being said, let’s talk foreign currencies and highlight an interesting trend.

Region by region, the currencies of the world are starting to differentiate themselves. Here’s what that looks like.

The Brazilian Real is gaining ground

The chart below shows a comparison of the Brazilian Real to the US dollar. Meaning how many real does $1 dollar buy. The real is up 7.64% YoY against the dollar.

The Brazilian central bank has been firm with their aggressive monetary tightening, and is aided by soaring commodity prices that help bolster their bottom line.

Key takeaway? Brazil exports more goods ($214b) than they import ($160b). High commodity prices actually help their economy survive through high interest rates set by the central bank. The high interest rates slow demand and help to control inflation, which strengthens their currency when comparing it to the rest of the world.

The Ruble is on a tear

The chart below shows a comparison of the Russian Ruble to the US dollar. Meaning how many rubles does $1 dollar buy. It just cruised through a 22 month high and is shrugging off the desired effects of worldwide sanctions. The ruble is up 8.15% YoY against the dollar.

According to Bloomberg, four European gas buyers have made ruble payments to Russia, and 10 more buyers have opened ruble accounts in preparation to do so. Source.

Just this morning, one of Germany’s largest energy firms, Uniper, said they are preparing to purchase Russian gas in rubles, and they’re not the only ones. Source. The process involves them selling euros for rubles, which is an important note we’ll touch on in the next section.

This is directly in contradiction with the EU sanctions, but Uniper stated “it is not possible to do without Russian gas in the short term.” Confusion over how to circumvent the EU sanctions will ensue, but the point remains that they will be circumvented, rendering the sanctions on Russian oil and gas useless.

Key takeaway? Russia has mandated that countries wishing to purchase Russian oil and gas must purchase it in rubles which increases demand, otherwise known as ‘buy pressure’ on the ruble itself. With Europe importing 41% of their natural gas from Russia, there is likely to be further demand for the ruble as countries are forced to keep the lights on.

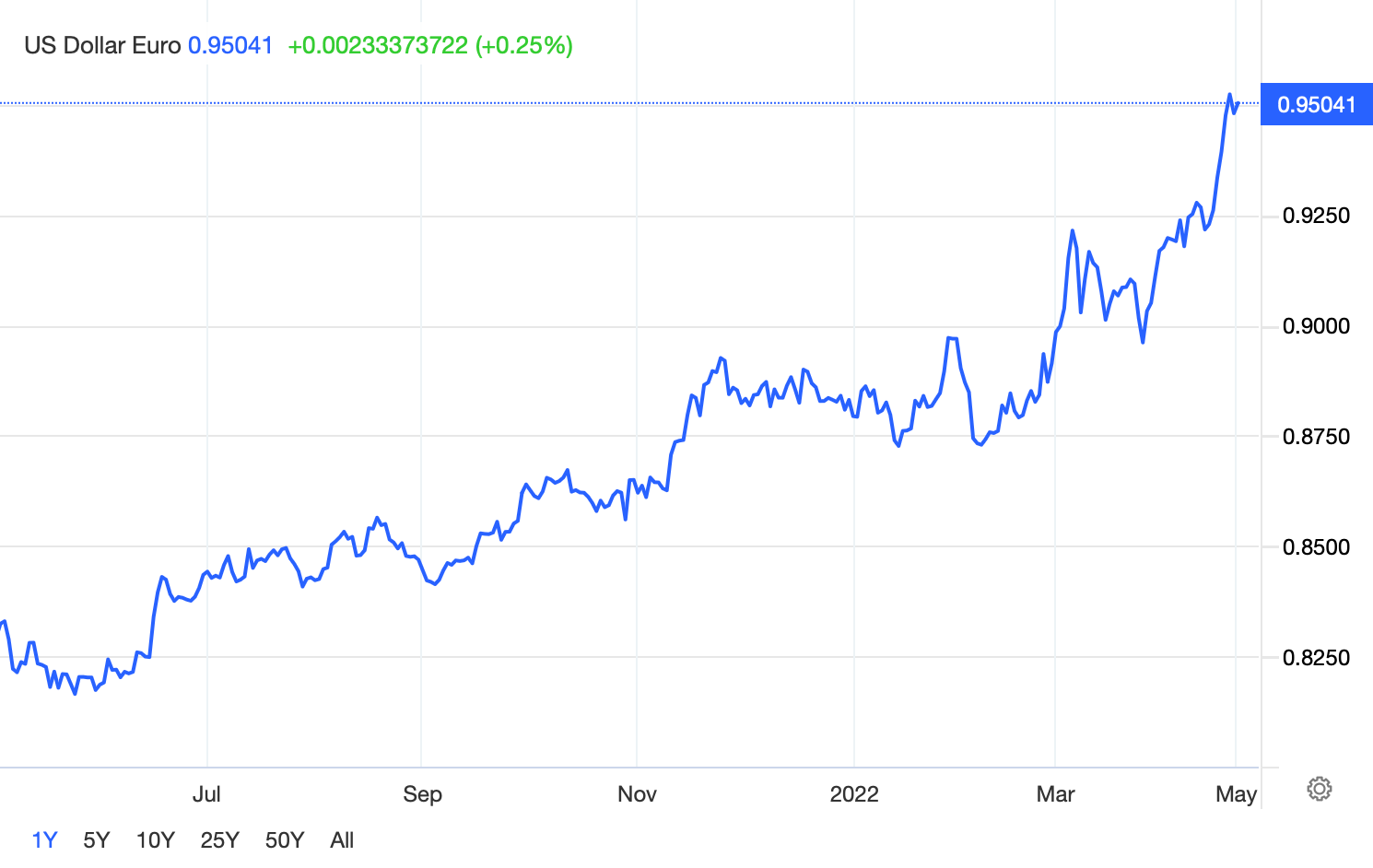

The Euro is tumbling

The chart below shows a comparison of the Euro to the US dollar. Meaning how many euros does $1 dollar buy. The euro is down 12.76% YoY compared to the dollar.

While the chart goes up, it means dollars buy more euros, or in other words, the euro is losing strength compared to the dollar.

As mentioned above, European companies and governments are being forced to sell euros for rubles to keep the lights on, putting ‘sell pressure’ on the euro and accelerating the decline. When mixed with other inflationary pressures, the euro is rapidly losing steam.

Key takeaway? As long as European countries are reliant on Russia for energy, they will be forced to sell euros to acquire rubles in order to purchase Russian oil and gas. This puts an enormous amount of sell pressure on the euro while strengthening the ruble. Combining this with inflationary pressures, the euro is weakening rapidly.

The Japanese Yen is in free fall

Finally, we made it to the Japanese yen. While telling the other currencies stories were important for a high level understanding, the yen is one currency that directly relates to the US dollar, for reasons you might not suspect.

The chart below shows a comparison of the yen to the US dollar. Meaning how many yen does $1 dollar buy. The yen is down 19.34% YoY compared to the dollar.

To understand the yen and its impact on the dollar, we must first understand the policy of the Japanese central bank, the Bank of Japan (BOJ).

The BOJ has been pursuing something called Yield Curve Control (YCC), a policy that results in them purchasing 10 year Japanese government bonds in any quantity in order to keep the yield at, or below, 0% (+- 25bps).

As a reader of the Decentralized Way, you’ll remember that bond prices and bond yields are inversely correlated, meaning as demand rises, yield falls, and vice versa.

The BOJ reinforced last week that they will buy an unlimited amount of 10 year Japanese government bonds in an attempt to maintain that 0% (+- 25bps) yield target.

To reiterate - The BOJ said they will print an unlimited amount of money to keep demand for the 10yr Japanese government bonds high enough to keep yield low.

Today, Japanese 10yr bonds are right at 0.25%. Meaning they’re exactly at the upper limit of the range and now the BOJ will attempt to create a steady flow of demand (via printing money) to keep the yield there.

The rationale behind this policy, according to BOJ Governor Haruhiko Kuroda, is that the bank must continue the massive stimulus program to support a fragile economic recovery and fight the deflationary pressures that have plagued Japan for the last 30 years. Source.

However, the unintended consequences of the pursuit of this monetary policy are compounding as bond yields rise worldwide.

Nobody wants Japanese bonds

And why would they?

As we’ve talked about previously, 10yr bond yields across the world are rising, with US 10yr treasuries hitting 2.9% as of writing.

As other 10yr bonds rise in yield, the Japanese 10yr becomes less and less enticing to hold to investors. The result? Investors part ways with their 10yr Japanese bonds and seek yield elsewhere. This puts even more downward pressure on the already declining yen.

The BOJ has a choice - Control their currency or control the 10yr bond. They’re opposites as far as monetary policy goes, so they cannot do both. They’re choosing the latter because the BOJ wants inflation. Japan has been battling deflation since 1990, which has slowed growth dramatically.

While Japan is the 4th largest export economy ($623b in 2020), they’re also the 5th largest import economy ($581b in 2020). Source.

In just the past 90 days, the yen has lost 19.8% of its value against the dollar. Meaning the goods that companies like Toyota need to produce cars have gotten 19.8% more expensive in just the last 90 days. Any imported goods in grocery stores have gotten 19.8% more expensive for consumers. You don’t need to be an economist to know that’s not great for business.

The only way out of the situation appears to be if bonds across the world decrease in yield, making the Japanese 10yr bonds more attractive to investors as they were over the last few years. However, with the US Fed putting quantitative tightening on the horizon, this outcome is highly unlikely in the near future as US yields are likely to increase.

One more important note here - The Japanese yen is the third most traded currency in the world, and commonly used as a store of value alongside the dollar and euro. Source. Weakening of the yen puts pressure on international trade in ways that we likely cannot even see yet.

Key takeaway? The yen is in trouble and the BOJ isn’t going to rescue it - they’re accelerating it by design. By artificially keeping 10yr bond yields low to encourage business spending, money will likely flow out of Japanese bonds, putting even more pressure on the yen.

The yen and the dollar

Finally, what you’ve been reading to see. Apologies for not getting to this sooner, but it’s vital to understand the macro environment that got us here.

Japan is the largest foreign holder of US debt, holding $1.32 billion worth of US Treasuries.

That’s important because our current economic framework looks something like this.

The Fed is lining up quantitative tightening (QT), which means they will no longer be purchasing billions worth of US treasuries every month (totaling nearly $6 trillion worth since March 2020), like they have over the last 2 years. Source. Result? Demand for bonds decreases.

The private sector looks at bonds and isn’t buying because why would you buy a bond that locks you in at 2.9% over 10 years when inflation is at (minimum) 8.5%? It makes no sense. Result? Demand for bonds decreases.

And it leaves Japan, the largest foreign holder of US debt, as one of the sole buyers of US treasuries left in the marketplace since their own 10yr bonds have next to no yield available. But what if Japanese bond yields began to actually rise? Japan would also likely keep their money at home, further decreasing the demand for bonds.

The result of all of this? US bond yields will likely continue to skyrocket until something breaks.

What will break first? Nobody knows. But at a certain point, something must give.

As the tweet below points out, our markets are built on collateral, in many cases rehypothecated collateral (meaning a single asset being used as collateral multiple times over).

If I loan you money and you give me an IOU for the worlds tastiest banana, but also borrow money from your best friend with an IOU for that same banana, and do that 5 more times… You get the idea. There’s still only 1 tasty banana but there’s 7 claims to it. What happens when all 7 of us want the banana you promised us?

And with that, we’ll see you in the next edition of the Decentralized Way.